Have you thought about selling your company or society this year? Do you know that there are important fiscal novelties that you should consider? As every year, the General State Budget Law has brought about a series of new tax developments both in terms of Personal Income Tax (IRPF) and Corporate Income Tax (Personal income tax). In this post, we tell you how the modification of the IS affects the taxation of the sale of a company and why it is important to have the help of a business consultancy expert in this type of corporate operations.

Taxation status of the sale of a company before 31-12-2021

Prior to the entry into force of the amendment introduced by the PGE, the taxation of the sale of a company was characterized by the fact that the double taxation exemption allowed companies to benefit from the 100% exemption of income from subsidiary companies at the headquarters of the parent company or holding company and provided the following advantages:

– Cash flow between group companies was exempt from taxation.

– The distribution of dividends from subsidiary to holding company had no tax cost.

– The distribution of excess cash from the subsidiary to the holding company was tax-free.

These three benefits occurred if the cash flow was within the group of companies, there was no company that could be considered a holding company benefiting from the double taxation exemption, and the money could be moved without taxation.

The cash flow makes it possible to diversify investment in other activities, to provide financing to the subsidiaries if they need it or to remove movable assets (excess cash) or real estate assets (real estate used for a different main activity), which any of the subsidiaries had in their assets, from business risk.

On the other hand, the future sale of any of the subsidiaries by the holding company was exempt from taxation if the holding company held less than 5% of the subsidiary and the holding company had been in existence for at least one year.

Therefore, the capital gain from the partial or total sale of the business to a third party was 100% exempt under Article 21 of the Corporate Income Tax Act.

Taxation of the sale of a company from 1 January 2021 with the new PGE (General Budget Law)

With the new General State Budget Law, section 1.a) of article 21 of the Corporate Income Tax Law is worded as follows:

1. Dividends or shares in the profits of entities shall be exempt when the following requirements are met:

a) That the percentage of direct or indirect participation in the capital or equity of the entity is at least 5 percent.

As a consequence of the above, with the application of the modification derived from the new PGE, the taxation of the sale of a company changes and from 1 January 2021 a limitation to the exemption is established and it is set at 95%. From this date, dividends will be taxed at 5%, which means that, in practice, the full amount of the dividend will be taxed at 1.25%.

The 100% exemption that existed before the amendment can only be applied in the case of companies that have created their first subsidiary after 1 January 2021 and have a turnover of less than 40 million euros. In practice, this will mean that the 100% exemption will hardly ever be applied and that, in general, 1.25% will be applied to dividends.

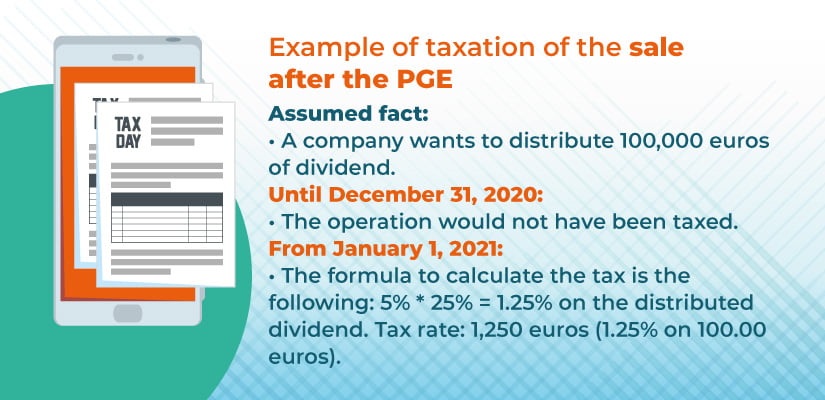

Practical example of taxation of the sale of a company before and after the amendment

In order to understand the implications of the change in taxation brought about by the amendment introduced by the PGE, let us give an example. Let’s start with the following assumption: a company wants to distribute a dividend of 100,000 euros.

Until 31 December 2020, the operation would not have been taxed, but with the modification of article 21 of the Corporate Income Tax Law, the formula for calculating taxation is as follows: 5% * 25% = 1.25% of the dividend distributed. The tax liability would therefore be 1,250 euros, which is the result of applying 1.25% on 100,000 euros.

As a result of all the above, it is essential to consult with expert business advice on the taxation of the sale of a company to avoid making mistakes and to be aware of the tax cost of the operation, as well as to find out about other formulas that can reduce the tax burden of companies.

Leialta website: https://www.leialta.com/en/

Blog for doing business in Spain: https://www.leialta.com/en/blog-for-doing-business-in-spain/

Linkedin: https://www.linkedin.com/company/leialta-s-l-/mycompany/