Did you know that you can start operating with your business in Spain in only a few weeks? You don’t need to create a commercial company, you just need to obtain a non-resident NIF (Tax Identification Number). In this post we will tell you what steps to follow in order to get it.

- Which forms must be submitted in order to apply for a non-resident NIF?

- What steps must the foreign company follow in order to obtain a NIF?

- What taxes will the non-resident company have to pay in Spain?

Which forms must be submitted in order to apply for a non-resident NIF?

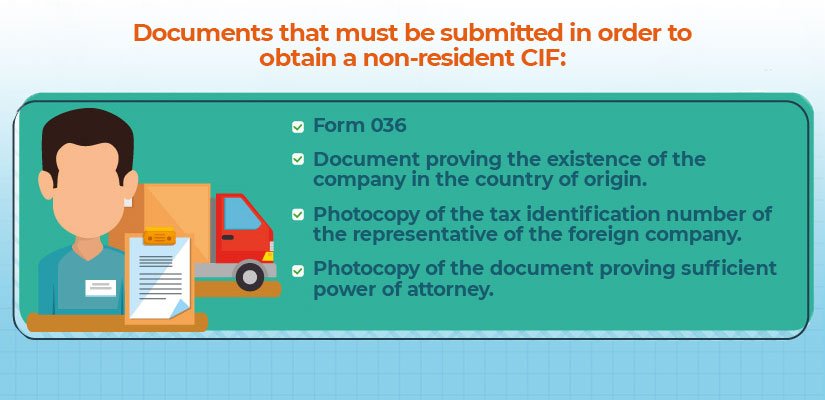

Any individual or legal entity that wants to do business in the territory of application of Spanish VAT must apply for a non-resident NIF. It is requested by the form 036, also called “Register of business persons, professionals and withholders – Register declaration for registration, modification and cancellation and simplified register declaration”.

In the event that the individual requesting the NIF number does not have a tax identification number assigned by the Tax Administration, he/she must apply for it by filing the form 030 “Tax register of parties liable for tax payments – Declaration of registration, change of address and/or variation in personal data in the tax register.“.

Both forms 036 and 030 can be found on the website of the Spanish Tax Agency: www.agenciatributaria.es.

What documentation is necessary to apply for the NIF of foreign legal entities?

In the case of foreign entities wishing to apply for the NIF, in addition to the forms we have seen, the following documents must be provided:

- Document that accredits that the company in the country of origin exists.

The document can be the deed of incorporation or the bylaws registered in an official registry. A certificate from a notary, a registry or a tax authority proving the existence of the company can also be submitted.

- Photocopy of the representative’s tax identification number.

The person signing the application form for the tax identification number on behalf of the company must attach a photocopy of the tax identification number issued by the Spanish administration.

- Photocopy of the document accrediting sufficient power of attorney.

In addition to all of the above, it must be demonstrated that the person submitting the documentation and the application has sufficient power of attorney to do so. This power of attorney may already be included in the document proving the existence of the company in the foreign country.

The documents we have mentioned above must be legalized with the Hague Apostille and translated by an official translator or through the Spanish Embassy or Consulate.

What steps must the foreign company follow in order to obtain a NIF?

The steps to obtain a non-resident NIF so that a foreign company can do business in Spain are simple:

- Write a power of attorney in favor of LEIALTA. The power of attorney is a public document that is granted before a Notary and allows LEIALTA to act on behalf of the foreign company in order to obtain the CIF. For the power of attorney to be valid, it must:

- Be granted by the administrative body of the foreign company (board of directors, sole administrator or joint and several or joint administrators).

- Include all the necessary powers so that all the steps to obtain the non-resident CIF and the electronic certificate can be carried out.

- Appoint a LEIALTA lawyer as the fiscal representative of the company in Spain. The fiscal representative must have fiscal residence in Spain, which means that he/she must live in Spain for at least 183 days a year.

- Incorporate the following data: name of the company, address, identification of the person signing, position held and date of appointment, identification of the attorney-in-fact (in this case, a LEIALTA partner) and definition of the powers granted depending on the service requested.

- Obtain the document proving the existence of the company in the country of origin.

- Include in the documents the Hague Apostille and send them to LEIALTA’s offices in Spain.

- Have all the documents translated by an official translator.

- Present the form 036 together with the documentation and obtain the CIF number.

If the foreign company that has obtained the CIF wishes to hire employees in Spain, it must also be registered in Social Security.

What taxes will the non-resident company have to pay in Spain?

The foreign company doing business in Spain through a non-resident CIF will not have to file and pay direct taxes such as the Corporate Income Tax (IS), since it is considered that it does not have a permanent physical place.

However, it will pay indirect taxes such as the Value Added Tax (VAT). VAT is declared monthly, quarterly (in the months of April, July, October and January) or annually (in January of each year a summary is presented).

In short, if you need to operate in Spain in a simple way, obtaining a non-resident CIF can be the solution. You will be able to start doing business in Spain soon and without having to comply with the tax, labor or mercantile obligations that you would have if you created a branch or a subsidiary.